The Rise of Stablecoins as Everyday Financial Instruments

The landscape of cryptocurrency is evolving, with stablecoins transitioning from mere trading tools to essential everyday financial instruments. According to the latest global research by BVNK, in collaboration with Coinbase and Artemis, there’s a noticeable shift in how users are incorporating dollar-pegged tokens into their financial strategies. This transformation is highlighted in The Stablecoin Utility Report 2026, which gathers insights from a survey comprising 4,658 adults across 15 countries. Findings reveal that over $300 billion in stablecoins is increasingly allocated for everyday activities such as payments, payroll, and savings—alongside traditional trading endeavors.

Stablecoins maintain a stable value as they are typically pegged 1:1 to fiat currencies like the U.S. dollar and supported by reserves or collateral. The circulating supply of this cryptocurrency segment stands around $300 billion, dominated by Tether’s (USDT) and Circle’s (USDC). The stablecoin market currently showcases vast potential as a financial tool that caters to users’ daily monetary needs, emphasizing its importance in personal finance management.

Growth in Savings Allocations

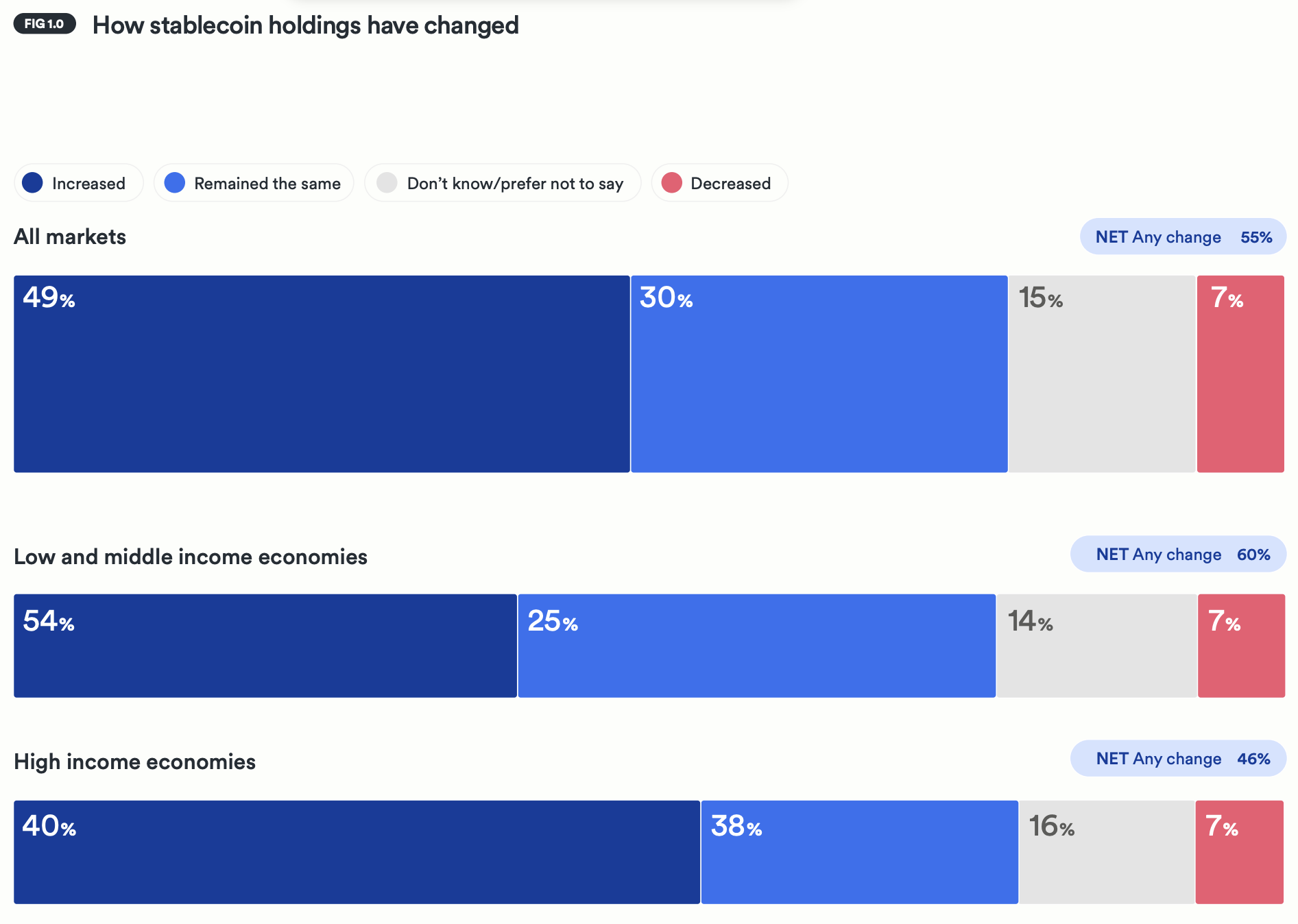

Notably, the report indicates that more than half of respondents have engaged with stablecoins over the past year, with 56% planning to buy more in the near future. Among those who haven’t yet ventured into stablecoin ownership, 13% expressed an intention to start utilizing these digital assets. There is a clear momentum, as many current stablecoin holders have increased their investments within the last year. On average, respondents allocate approximately one-third of their total savings to cryptocurrencies, with a significant portion directed towards stablecoins.

In regions characterized by volatile local currencies or unreliable cross-border payment options, the inclination towards stablecoins is even more pronounced. The study highlights that users in low- and middle-income countries exhibit higher ownership rates compared to those in affluent markets, with Africa emerging as a leader in future stablecoin adoption. Such trends align with estimates from Standard Chartered, suggesting that potentially $1 trillion could shift from emerging market bank deposits to dollar-backed stablecoins.

Spending Habits and Cross-Border Transactions

Stablecoins are not merely sitting idle; they actively circulate within the economy. Data from the survey reveals that 27% of holders spend stablecoins directly on goods and services, while 45% choose to convert them into local currencies. Many users act quickly, with over one-quarter converting or spending their stablecoins within days and nearly two-thirds doing so within a few months. The demand for businesses to accept stablecoin payments exceeds the current capacity, as 52% of holders reported making purchases specifically because a vendor accepted stablecoins.

For freelancers and gig workers, stablecoins play a crucial role in their financial ecosystem. On average, these tokens account for approximately 35% of their annual earnings. Many reported enhanced capabilities to work with international clients, leading to increased sales volumes and expanded customerbases. Significant cost savings further incentivize this behavior; recipients of stablecoin payments and remittances enjoy average fee savings of around 40% compared to traditional payment solutions.

Challenges in Stablecoin Adoption

Despite the promising statistics, the report reveals certain challenges hindering widespread adoption. Users often encounter frustrations such as irreversible payments, risks of losing funds, and complicated transaction processes. Confusion surrounding blockchain selection and wallet management further complicates the user experience. Many users are calling for stablecoin transaction processes to align more closely with traditional payment systems—desiring universal acceptance, clearer fee structures, and enhanced consumer protections.

In response to these challenges, there is a growing demand for a “connective layer” that can seamlessly bridge traditional finance and digital currencies. If achieved, stablecoins could function less as speculative assets and more as digital cash—programmable, borderless, and regarded as straightforward money by an expanding user base.

Regulatory Environment for Stablecoins

As the stablecoin sector matures, regulatory clarity is becoming increasingly important, particularly in the United States. The findings coincide with advancements in regulations under President Trump’s administration, such as the recent signing of the GENIUS ACT into law. Policymakers are working towards a comprehensive federal framework for the cryptocurrency market, incorporating regulations specific to dollar-backed tokens.

Due to the importance of stablecoins, discussions around their yields are intensifying, with industry insiders noting that the “clock is ticking” to establish rules before upcoming crucial electoral cycles. Clear regulatory guidance may pave the way for broader acceptance and use of stablecoins, further solidifying their role in everyday financial transactions.

Conclusion: A New Era for Stablecoins

In summary, stablecoins are on a trajectory to redefine their role in personal finance, shifting from speculative trading tools to integral components of daily financial management. With more users recognizing the utility of stablecoins for savings, spending, and international transactions, the implications for the global financial landscape are significant.

The data reveals a confluence of factors driving adoption, particularly in regions facing economic volatility. As financial systems evolve, overcoming existing challenges and establishing comprehensive regulatory frameworks will be vital in ensuring stablecoins can fulfill their potential as seamless, digital financial instruments. The future could witness a world where stablecoins are as ubiquitous as traditional currencies, fundamentally altering how individuals manage their finances.