The Growing Challenge of Stablecoin Adoption for U.S. Banks

Recent insights from Standard Chartered have revealed that U.S. banks could face as much as $500 billion in deposit outflows to stablecoins by 2028. This staggering figure frames stablecoin adoption as not just a trend, but a structural risk to the traditional banking system. As the stablecoin market cap grows—a projected $2 trillion by the end of the decade—this shift could represent nearly one-third of that total. Moreover, about half of the $1 trillion forecasted migration of deposits from emerging markets to U.S. dollar stablecoins underscores the urgency for financial institutions to adapt.

Assessing the Risks for Banks

Geoffrey Kendrick, Standard Chartered’s global head of digital assets research, emphasizes that the risks associated with this migration are becoming increasingly evident. The transition toward blockchain-based payment systems is altering the landscape of core banking activities. The delays surrounding legislative efforts such as the U.S. Digital Asset Market Clarity Act only add to the confusion. This regulatory uncertainty could either hinder or, conversely, accelerate stablecoin adoption once a framework is finalized. Notably, discussions within Washington have seen significant players, including large banks and crypto exchange Coinbase, clashing over regulations that could shape the future of stablecoin usage.

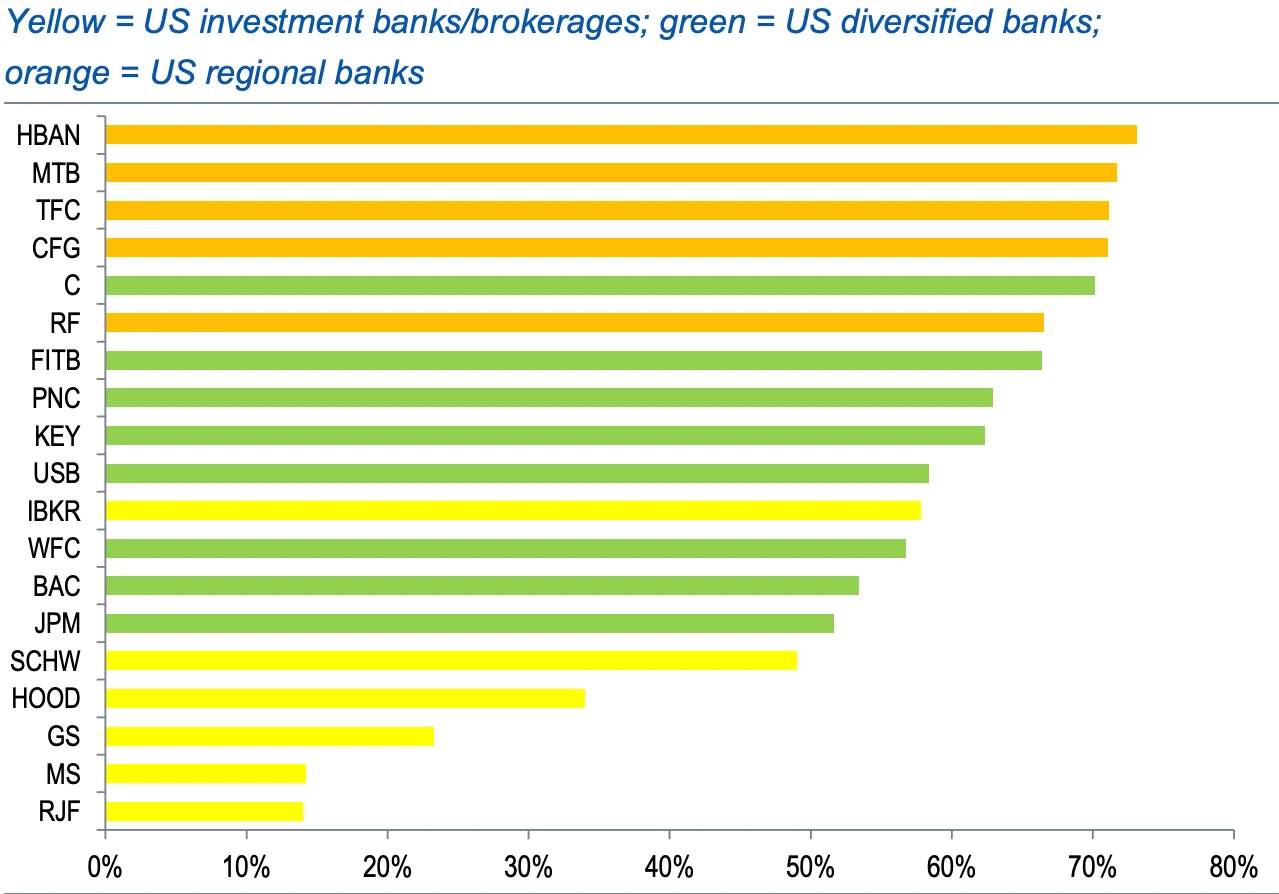

Regional Banks and Vulnerability

To pinpoint which banks are most at risk, Standard Chartered analyzed net interest margin (NIM) income as a percentage of total revenue. This metric offers insight into vulnerability to deposit flight, as deposits are crucial for generating net interest income. The findings indicate that U.S. regional banks exhibit the highest risk due to their heavy reliance on deposit-driven lending. In contrast, diversified banks face moderate risks, while investment banks and brokerages, which are less dependent on deposits, show the least exposure.

Structural Factors Amplifying Risk

The report identifies various structural factors that could heighten deposit losses. Currently, the two leading stablecoin issuers—Tether and Circle—hold a minimal portion of their reserves in traditional bank deposits, which limits their potential to reinject funds back into the banking system. Standard Chartered notes that approximately two-thirds of current stablecoin demand originates from emerging markets. This presents a stark contrast to the one-third tied to developed markets, reinforcing the prediction of $500 billion in outflows impacting U.S. and other developed-economy banks.

Uneven Disruption Across the Sector

While it’s clear that some banks will suffer more than others due to stablecoin disruptions, the overall impact will depend on individual responses. Banks that adapt their funding models or engage more directly with tokenized financial infrastructures will likely fare better. Standard Chartered cautions that the effects of this transition could extend beyond deposit losses, potentially threatening non-interest income as the tokenization of physical assets becomes more common.

The Path Forward for U.S. Banks

As of now, U.S. dollar-denominated stablecoins constitute around $300 billion in supply. If the projections by Standard Chartered hold true, we could see the market tripling in size, nearing the anticipated $1 trillion mark by 2028 purely from bank deposits. This looming transformation highlights the need for financial institutions to innovate and stay ahead of emerging trends to mitigate the risks posed by stablecoin adoption. By addressing regulatory challenges and adapting to the evolving landscape, banks can position themselves to thrive in a future that increasingly embraces digital currencies and blockchain technology.

In conclusion, the emerging dominance of stablecoins is set to redefine financial landscapes, making it crucial for U.S. banks to strategically navigate this shift. Understanding the potential impacts and adopting proactive measures could determine their resilience in an evolving financial ecosystem.