The Decline of Bitcoin Treasury Companies: An In-Depth Analysis

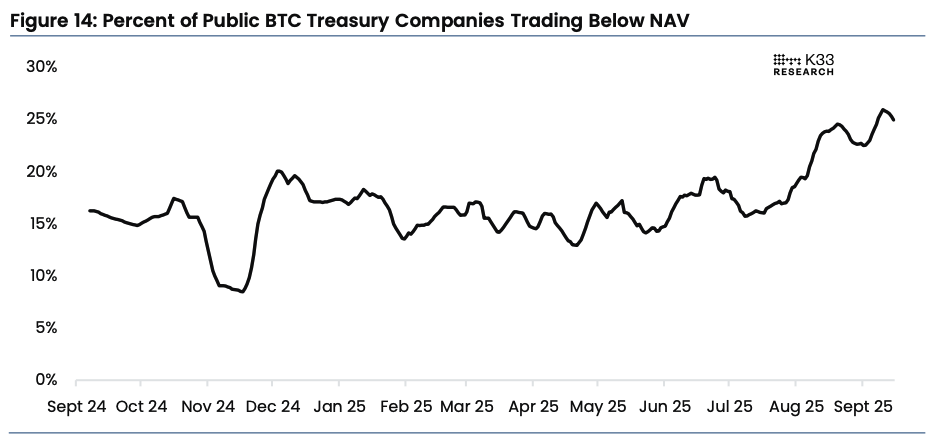

The landscape surrounding Bitcoin treasury companies is undergoing significant changes, indicating a slowdown in their growth and market prominence. Recent data from K33 reveals that approximately 25% of these publicly traded entities are now valued below the actual Bitcoin they hold. This shift has alarming implications for future capital raising and acquisition strategies. Understanding the mechanics behind these market movements can offer investors and stakeholders crucial insights into the evolving cryptocurrency landscape.

The Impact of Market Valuation on Bitcoin Treasuries

A critical factor in the performance of Bitcoin treasury companies is their market-to-net-asset-value (mNAV). According to K33’s Head of Research Vetle Lunde, when companies trade below their NAV, issuing new shares becomes dilutive. This process effectively transfers more ownership to new investors than the monetary value the company gains in return, making it an unfavorable scenario for existing shareholders. The recent decline in multiple valuations emphasizes the pressures faced by these entities, as the market is beginning to reflect a more cautious approach to cryptocurrency investments.

Notable Failures and Market Trends

The downturn has been particularly pronounced for certain companies. For instance, the merger entity KindlyMD and Nakamoto Holdings (NAKA) has seen a staggering 96% drop in its market value, with its mNAV multiple falling from 75 to just 0.7. Other companies such as Tether-backed Twenty One, Semler Scientific, and The Smarter Web Company are also experiencing a decline in their mNAV, currently sitting below 1. While larger firms continue to trade at premiums, the distribution of valuations is increasingly skewed, with smaller firms struggling to maintain their foothold.

Diminished Demand from Major Players

Prominent figures in the Bitcoin treasury space, such as Michael Saylor from MicroStrategy (MSTR), are also experiencing a decline in their market premium. As of March 2024, MSTR’s premium has fallen to 1.26, the lowest in recent months, limiting its capacity to raise funds for further Bitcoin acquisitions. This dwindling premium reflects a broader reduction in demand from one of the sector’s essential buyers and raises concerns about the future appetite for Bitcoin within corporate treasuries.

Shifting Acquisition Patterns

The declining market and premium values have begun to manifest in actual acquisition rates. Data indicates that Bitcoin treasury companies are currently purchasing an average of only 1,428 BTC daily, a drop that represents the lowest trading pace since May. This reduction indicates that the once boisterous zeal for corporate acquisitions is beginning to fade. Lunde contends that treasury firms should ideally not trade at a premium over their balance sheets due to the inherent financial burdens like advisory fees and complex capital structures.

The Return to Organic Demand

Given the significant public treasury holdings surpassing 1 million BTC, the market appears to be transitioning back to natural demand drivers, such as Exchange-Traded Funds (ETFs) and retail investors. In the face of corporate treasuries losing their stronghold on marginal demand, the crypto economy may be finding a new equilibrium characterized by diversifying investment sources. This shift suggests a more grounded approach to Bitcoin investments, steering clear of volatility driven by corporate treasury speculation.

Bitcoin Futures and Market Equilibrium

In parallel, the dynamics of Bitcoin futures trading are also undergoing a transformation. Recent reports indicate that CME Bitcoin futures are once again trading at modest premiums against offshore perpetual contracts, suggesting a more stable market condition. As discounts traditionally correlate with market peaks, the current state hints at a healthier balance of institutional flows, which are helping to anchor CME prices closer to the spot price of Bitcoin.

Future Financing Risks

However, the funding rates remain elevated, averaging nearly 6% over the past week, exceeding the 5.4% yearly average. This scenario, combined with a high level of open interest in perpetual contracts, indicates an ongoing long bias among highly leveraged participants. While this could lead to an eventual squeeze of over-exposed longs, the current balance between premiums and funding rates suggests a less unnaturally inflated market compared to instances when Bitcoin previously traded above $115,000.

Conclusion: Navigating a Changing Landscape

In summary, the retreat in Bitcoin treasury market valuations and the challenges faced by prominent corporate players raise important questions about the future of Bitcoin as a treasury asset. As the crypto market evolves, the focus may shift from corporate to more organic buyer behaviors. Stakeholders are thus advised to approach investments with caution, recognizing the potential for volatility and changing demand dynamics as they navigate this shifting landscape. Furthermore, the need for strategic reevaluations among Bitcoin treasury firms could pave the way for a healthier and more sustainable market in the long run.